Earnings Reports (April 29th-May 3rd)

Taking a Look at Earnings Results for Lemonade (LMND) & Relay Therapeutics (RLAY).

Today’s Newsletter is Powered by The Bear Report!

The Bear Report is a YouTube Channel dedicated to offering unbiased, bi-weekly analysis of companies with potentially bearish outlooks. Their mission is to equip both bears and bulls with comprehensive information, fostering an understanding of all facets of a business's investment thesis.

Embracing open-mindedness is crucial for any investor, whether bull or bear. Recognizing the importance of seeing both sides of an investment is what distinguishes the great investors from the merely good.

By subscribing, you'll gain access to bi-weekly, in-depth presentations on publicly traded companies, complemented by a variety of concise, short form videos.

You can subscribe below here:

If this has issues connecting to their channel, simply search @TheBearReport in the YouTube search bar.

1. Lemonade (LMND)

This past week, Lemonade (LMND) released their Q1 2024 earnings, delivering exciting news about their accelerated timeline for cash flow positivity:

Demand and Growth Insights

Performance Overview: The company has outperformed In Force Premium (IFP) guidance by 0.5%, with a 64% 2-year revenue Compound Annual Growth Rate (CAGR), a slight decline from previous quarters. Gross earned premium exceeded expectations by 2.2%, and revenue beat estimates by 5% and guidance by 6.3%.

Factors Influencing Revenue: This quarter's revenue boost was partially aided by reserve releases/adjustments due to improved loss rate assumptions, somewhat analogous to credit reserve level adjustments for lenders. Additional boosts came from ceded reinsurance premium commission favorability and increased net interest income, which is becoming a more significant component of the business as the cash reserves grow.

Customer and Product Insights: The company saw stronger dollar retention gains fueled by a more comprehensive product suite across states. Premium per customer growth was driven mainly by rate increases rather than past strategies of shifting to higher premium buckets, as observed with products like auto and home insurance.

Margins and Profitability

Financial Metrics: EBITDA and gross profit margin exceeded estimates by 17% and 20% respectively, with overall losses and expenses lower than anticipated. Operational expenditures increased by only 2% YoY, while other insurance expenses grew due to heightened regulatory activity.

Cost Management: General and administrative expenses decreased by 9% YoY due to reduced headcount, and R&D expenses were down by 4%. Improved gross margins were attributed to declining loss ratios.

Balance Sheet and Annual Guidance

Liquidity and Debt: The company maintains a robust balance sheet with $927 million in cash and equivalents, and no debt. Share dilution was minimal at 1.3% YoY.

Forward-Looking Statements: IFP guidance was reiterated, while Gross Earned Premium (GEP) and revenue guidance were slightly raised. EBITDA expectations were also adjusted upward due to improving operational efficiencies and new growth opportunities signaled by management.

Strategic Developments and Future Outlook

Regulatory and Market Dynamics: Premium rate filing approvals have started to accelerate, particularly in significant markets like California, positioning the company to expand originations profitably. Management remains proactive in navigating inflation impacts and regulatory environments to sustain growth.

Innovation and Competitive Edge: Lemonade continues to leverage its tech-native, AI-driven infrastructure to enhance customer service and operational efficiency. This strategic focus is reflected in favorable cost-to-serve metrics and loss adjustment expenses, underscoring a competitive advantage in a traditionally challenging market.

Net Cash Positive Movement: The company is advancing its timeline to achieve net cash flow positivity from early 2025 to late 2024, benefiting significantly from its synthetic agent program.

Management Commentary

Executive Insights: Co-CEO Daniel Schreiber remarked on the healthy pace of rate approvals and the optimistic trajectory in larger markets. The focus remains on refining the auto insurance model, with expectations to scale up in early 2025.

Reinsurance and Market Positioning: With improving loss ratio trends and a more diversified portfolio, upcoming reinsurance negotiations are anticipated to yield favorable terms, enhancing Lemonade's market position.

My Take

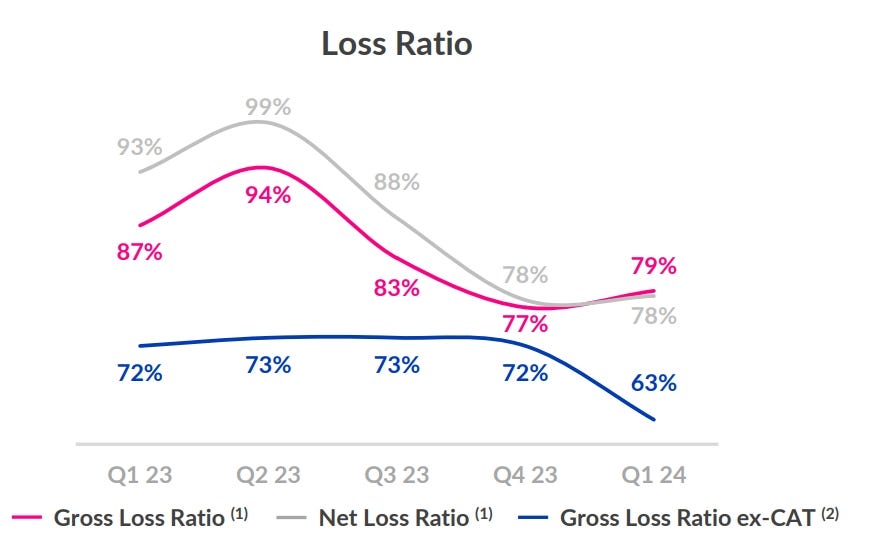

The company performed exceptionally well this quarter, despite this period typically experiencing lighter seasonality. LMND is showing significant progress across their key metrics, which is very promising. Two standout developments for me were the accelerated timeline for achieving cash flow positivity by late 2024 and the reduction of their Ex-CAT ratio to 63%.

.

Initially, there was considerable skepticism regarding their customer cortex, with critics arguing that it led to poor underwriting. However, it now seems that the company's AI is functioning as intended, providing a much clearer operational picture. It's important to recognize that LMND represents a long-term investment. If they maintain their current trajectory, the potential returns in the coming years could be substantial.

I want to emphasize a critical point that many beginners overlook but distinguishes truly savvy investors: by the time LMND reaches its profitability and cash flow targets, its share price will likely command a significant premium over today's levels. Investing with vision, conviction, and trust is essential. This isn't just irrational enthusiasm for LMND, given that they still have considerable challenges ahead. However, at moments like these—when doubts about the prevailing narrative peak—it's an opportune time to consider increasing one’s investment, assuming they continue to execute as they have. As for my position, I'm comfortable with my current investment in LMND, but should the stock continue to hover at these levels, I might be inclined to increase my stake.

2. Relay Therapeutics (RLAY)

RLAY announced a business update this past week for Q1 2024:

Financial Performance

Cash Position: As of March 31, 2024, RLAY reported a solid financial position with $749.6M in cash, cash equivalents, and investments, slightly down from $750.1M at the end of 2023. This robust financial standing is projected to fund operations into the second half of 2026, providing a substantial runway for ongoing and future projects.

Revenue: There was an increase in revenue, rising to $10M in Q1 2024 from just $0.2M in Q1 2023. This surge was primarily driven by a $10M milestone payment from the collaboration and license agreement with Genentech, reflecting significant progress in their partnered projects.

Expenses: Research and development expenses slightly decreased to $82.4M from $82.8M YoY, aligning with the company’s strategic prioritization of its pipeline. General and administrative expenses increased modestly to $19.8M, primarily due to higher stock compensation expenses.

Net Loss: The net loss improved to $81.4M ($0.62 per share) from $94.2M ($0.78 per share) in the previous year, indicating better operational efficiency and control over expenses.

Operational Highlights

Clinical Development: The RLY-2608 development program remains a cornerstone of Relay’s portfolio, with ongoing patient enrollment in studies targeting PI3Kα-mutant, HR+, HER2- breast cancer. The company anticipates providing a data update in the latter half of 2024, potentially enhancing the drug’s profile.

Strategic Focus: Resource allocation in 2024 has been adjusted to allow data from the Lirafugratinib (RLY-4008) studies to mature, informing future clinical development paths. This strategic decision underscores Relay’s commitment to data-driven development strategies.

Pipeline Expansion: Anticipation builds as Relay Therapeutics plans to unveil at least one new pre-clinical program in 2024 with first-in-class potential, expanding its innovative portfolio.

Future Outlook and Milestones

RLY-2608 Updates: Updates on the RLY-2608 plus fulvestrant combinations are expected in the second half of the year, along with initial safety data from the RLY-2608 plus fulvestrant plus ribociclib trials.

Lirafugratinib Developments: A regulatory and tumor-agnostic data update is anticipated, which could significantly influence the drug’s clinical trajectory.

Pre-Clinical Programs: The disclosure of new programs will likely provide fresh insights into Relay’s expanding research scope.

My Take

Currently, there's not much new activity with RLAY until they release additional data from their clinical trials, expected later this year. I plan to maintain my position in RLAY as my conviction in their potential remains unchanged.