Earnings Reports (November 6th-10th)

Taking a Look at Earnings Reports for Coherus BioSciences, Upstart, & Global Crossing Airlines.

This week's agenda is packed with report analyses, including Coherus BioSciences (CHRS), Upstart (UPST), and Global Crossings Airlines (JETMF). Each of these holdings represents a calculated risk within my portfolio. Unfortunately, both CHRS and UPST experienced dramatic declines post-earnings, which sent shockwaves through the market. The downturn in CHRS, while significant, aligns with expectations to a degree. However, the performance of UPST can only be described as deeply disappointing. As I continue to evaluate UPST's situation, my goal is to crystallize my thoughts and strategize effectively. I aim to share these insights and strategies with fellow investors who find themselves navigating similar challenges. Let’s dive in!

1. Coherus BioSciences (CHRS)

CHRS recently unveiled material that, upon thorough analysis, holds considerable promise for investors. Admittedly, the initial reaction to the less-than-stellar Yusimry figures, alongside revenue shortfalls and guarded forecasts, may seem disheartening. Yet, for those who anticipated such outcomes, the continued decline in CHRS's stock price may appear to be an overreaction.

Navigating the complexities of CHRS's market position is no small feat. However, despite the unique landscape, the company remains on a clear path to achieve cash flow positivity by 2024. Furthermore, CHRS has been consistently gaining market share QoQ through its expanded product offerings. This momentum underscores a strategic advancement that could well merit a closer look from those invested in its journey.

Key Financial Highlights:

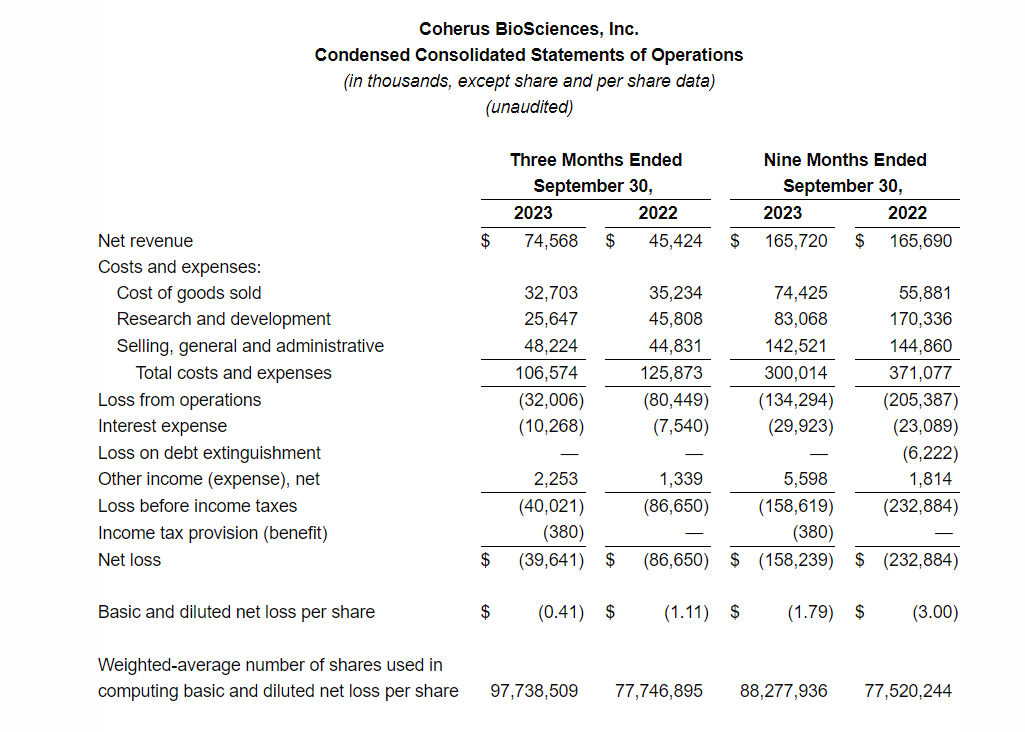

Net Revenue:

Total for Q3 2023 is $74.6M.

Breakdown includes UDENYCA sales at $33M, CIMERLI sales at $40M, and YUSIMRY sales at $1.4M (launched July 3, 2023, not as underwhelming as you should think… ramp-ups take time).

In comparison to Q3 2022, there was an increase from $45.4M, which consisted primarily of UDENYCA sales.

Year-to-Date Revenue:

Remains consistent at $165.7M for the nine months of both 2023 and 2022.

Cost of Goods Sold (COGS):

Q3 2023 COGS were $32.7M, a decrease from $35.2M in Q3 2022.

Nine-month COGS rose to $74.4M in 2023 from $55.9M in 2022.

Includes royalty payments for UDENYCA and significant royalties on CIMERLI gross profits.

Research and Development (R&D) Expenses:

Dropped to $25.6M in Q3 2023 from $45.8M in Q3 2022.

For the nine months, R&D expenses were $83.1M in 2023, a reduction from $170.3M in 2022.

Selling, General and Administrative (SG&A) Expenses:

Slightly increased to $48.2M in Q3 2023 from $44.8M in Q3 2022.

Nine-month SG&A expenses were $142.5M in 2023, slightly less than $144.9M in 2022.

Net Loss:

Q3 2023 saw a net loss of $39.6M, improved from a net loss of $86.7M in Q3 2022.

Nine-month net loss was $158.2M in 2023, better than the $232.9M loss in 2022.

Non-GAAP Net Loss:

For Q3 2023, the non-GAAP net loss was $26.9M, compared to a non-GAAP net loss of $74.4M for Q3 2022.

The nine-month non-GAAP net loss totaled $117.3 million in 2023, an improvement from $187.7 million in 2022.

Liquidity:

Cash, cash equivalents, and marketable securities stood at $131.1M as of September 30, 2023, down from $191.7M at the end of 2022.

2023 Revenue and Expense Guidance:

Revenue Guidance:

Lowered to a range of $250M to $260M due to delays in commercial launches (this should have been expected with Toripalimab and UDENCYA OBI).

R&D and SG&A Expense Guidance:

Adjusted to a range of $300M to $310M, which includes significant stock-based compensation and excludes Surface Oncology acquisition costs.

At first glance, the results might appear disappointing, with revenue falling short of expectations and a downward revision in guidance. However, this view is incomplete without considering the reasons behind these figures. It’s essential to understand the factors that contributed to the revenue shortfall, including the lowered guidance.

Furthermore, it’s important to recognize the promising trajectory of YUSIMRY, which has only recently entered the market. Like many new products, YUSIMRY is poised to gradually capture market share as it gains momentum. The initial uptake of a new product often doesn't reflect its long-term potential, and YUSIMRY's ramp-up period is a crucial phase where strategic investments today can lead to significant market inroads tomorrow.

The potential for growth in market share with YUSIMRY, alongside other products like LOQTORZI (Toripalimab), is an important aspect that must be considered when evaluating the company’s current financial results and future prospects.

Product Performances & Updates

CIMERLI:

Achieved $40M in sales in Q3 2023, a significant increase from $26.7M in Q2.

Surpassed 100,000 doses sold since its launch on October 3, 2022.

Acquired a 29% market share in the ranibizumab market by Q3 2023 (this is huge).

UDENYCA:

Sales rose to $33M in Q3 2023, up from $31.7M in the previous quarter.

Market share increased to 16.5%, with a growth of 4.3 percentage points from Q2 (Their products are taking significant market share).

The autoinjector presentation has been ordered by over 250 accounts since its May 2023 launch.

Improved formulary coverage expected to boost demand further in Q4 2023 and into 2024.

The resubmitted Biologics License Application for UDENYCA ONBODY is awaiting potential FDA approval in late 2023 or early 2024 (this is part of the revenue miss and revised guidance).

LOQTORZI:

FDA approved for first-line treatment of certain types of nasopharyngeal carcinoma on October 27, 2023.

Scheduled for commercial launch in Q1 2024 (I think this has potential to make a large impact).

Showcased at prominent conferences, highlighting its innovative mechanism of action.

YUSIMRY:

Launched on July 3, 2023, as a Humira biosimilar with a user-friendly autoinjector.

Now available nationwide across retail, mail order, and specialty pharmacy channels.

Surface Oncology Acquisition & Pipeline Developments:

Coherus completed the acquisition of Surface Oncology on September 8, 2023, enhancing its immuno-oncology pipeline.

Presented new data for anti-IL-27 and anti-CCR8 antibodies at the 38th Annual SITC meeting.

Plans to file an IND application for a novel ILT4-targeted antibody (CHS-1000) in Q1 2024.

It's important to highlight a few key points to better understand the company's trajectory. Firstly, YUSIMRY is a notable recent addition to the company's portfolio, already forging strategic partnerships and accelerating its efforts to capture market share. Meanwhile, significant upcoming milestones include the anticipated 2024 launch of LOQTORZI and the potential late 2023 to early 2024 FDA approval of UDENYCA OBI. These events represent critical catalysts that seem to be undervalued currently.

However, it must be acknowledged that delays in the development and approval of these products have had an adverse impact on the company's stock price. Despite these setbacks, the management has consistently pointed out that, assuming no further delays, the company is on track to achieve positive cash flow in 2024. This underscores the importance of maintaining the planned timelines to realize the company’s financial goals.

My Take

If we take a step back and really look at what's going on, it seems like there's a good chance to buy into this company at a good price. I've been really positive about this company for a long time—since the price was less than $5 per share. With some big developments coming up and the company's drugs starting to grab more of the market, this could turn out to be a really smart bet. We just need to hang tight and give the company's leaders time to do their thing and let our plan come to life.

Now, it's not all sunshine and rainbows. If the newly launched YUSIMRY doesn't do well, or if LOQTORZI doesn't get off to a good start in 2024, or if there are more hold-ups with getting UDENYCA OBI out the door, the company might hit some rough waters. They might even have to dilute shareholders to get some cash, but honestly, I don't see it going that way. For me, I'm looking at this as my chance to buy more shares. With the stock price where it is now, I think it's a low-risk bet with the potential for a big payoff. Now's the time to go against the crowd and grab this opportunity.

2. Upstart (UPST)

Let's face it, the last quarter was a disaster. It stings even more when you look across the fence and see a rival like Pagaya Technologies not just meeting, but smashing expectations with their highest revenues ever. This raises a couple of troubling questions: Is Pagaya playing with their books, or is UPST simply missing the mark? If it's the latter, it might be time to shake up the team at the top.

Thinking about this deeply is unsettling, especially when you consider the prospect of a real downturn. If UPST is struggling now, in relatively stable times, how will they fare when the economy really hits a rough patch? (Okay, end of rant.)

But it wasn't all doom and gloom this quarter. UPST did see some positives—an increase in automation, they onboarded new partners, and the default rates are on the decline. Their technology seems to be doing its job, so what gives? Let's get into the details and really unpack what's happening.

Key Financial Highlights:

Revenue Insights

The quarter saw a total revenue of $135M, marking a decline of 14% from the third quarter of the previous year.

Fee revenue also dipped to $147M, down 18% compared to the same period last year.

Operational Metrics

Loan originations by lending partners reached 114,464, amounting to $1.2B on the platform, a 34% decrease from the third quarter of 2022.

The conversion rate on rate requests slightly fell to 9.5%, a marginal drop from 9.7% YoY.

Profitability and Earnings

The loss from operations improved to ($43.8)M, better than the loss of ($58.1)M YoY.

GAAP net loss showed improvement at ($40.3)M, up from a loss of ($56.2)M in the prior year’s quarter.

The adjusted net loss was ($3.9)M, which is an improvement from the previous year’s ($19.3)M.

GAAP diluted EPS was at ($0.48), and the adjusted diluted EPS stood at ($0.05).

Profit Contribution and EBITDA

Contribution profit was reported at $94.2M, a slight 2% YoY decrease, but with a contribution margin increase to 64% from 54%.

Adjusted EBITDA turned positive at $2.3M, a significant improvement from a ($14.4)M loss, with the adjusted EBITDA margin improving to 2% of total revenue from the previous negative margin of (9%).

The recent quarter presented significant challenges for UPST, compounded by a concerning lack of transparency from the management team. Yikes.

Financial Outlook

Revenue Breakdown:

Total Revenue: Approximately $135M.

Fee-Based Revenue: Approximately $150M.

Net Interest Income (Loss): Approximately ($15M).

Profitability Metrics:

Contribution Margin: Roughly 62%.

Net Income (Loss): Approximately ($48M).

Adjusted Net Income (Loss): Approximately ($14M).

Adjusted EBITDA: Break-even at approximately $0.

Share Information:

Basic Weighted-Average Shares Outstanding: Roughly 85.6 million.

Diluted Weighted-Average Shares Outstanding: Also about 85.6 million.

My Take

While it's clear that this quarter was disappointing for UPST, there's no point in dwelling on the negatives. However, it's important to recognize that the market UPST operates in isn't a 'winner takes all' scenario. That said, UPST's noticeable lag behind its competitors raises some serious concerns about the company's resilience and overall strategy. It's undeniable that UPST is intricately linked to the fluctuations of the credit cycle and the movement of interest rates. Although this can account for some of the challenges faced, it's not a perennial shield against underperformance, especially when counterparts are managing to excel under the same conditions.

The crux of the matter may lie with the company's leadership. There's a growing sense that a change in management could be the pivot UPST needs to navigate back to smoother waters — a possibility that remains within reach.

As for the long-term potential of UPST, it remains intact. But it's this potential that's now at odds with my dwindling conviction. Holding on for a turnaround is a gamble, and as I weigh my options, the balance between holding and selling is tipping. Given that my cost basis hovers just above $17 per share, the decision on whether to continue riding out the storm or to seek shelter is becoming increasingly pressing.

3. Global Crossing Airlines (JETMF)

Before diving into the specifics, it's crucial for investors to understand that we're examining a relatively obscure stock here: JETMF. It's under-the-radar, lacking analyst coverage, and comes with lower liquidity. That being said, JETMF has delivered another remarkable quarter. The company recorded an all-time high in block hours, maintained robust revenue, and the management's strategies for growth have consistently exceeded my expectations.

Key Financial Highlights:

Revenue: Generated $42.6M, reflecting the company's strong performance.

EBITDAR: Achieved $7.6M, underscoring operational profitability.

Operational Metrics:

Block Hours: Saw a significant increase, soaring 173% over the second quarter of 2022.

Aircraft Utilization: Jumped by 50%, indicating more efficient use of assets.

Workforce Expansion: The pilot roster expanded to 125, supporting the increased flight operations.

Strategic and Operational Developments:

Secured a financial boost with a $35M debt facility from Axar Capital.

Expanded the fleet, signing Letters of Intent (LOIs) for three additional aircraft: two A320s and one A321.

Doubled our pilot headcount to 120, ensuring ample crew for increased operations.

Delivered impressive flight hours, with over 1,800 block hours wet leased to TUI, a major European leisure carrier.

Enhanced VIP travel options by taking delivery of an A319 aircraft configured with 68 luxury seats.

Experienced a surge in demand from government contracts, highlighting our versatility in service offerings.

Strengthened our cargo operations with the introduction of a third A321 freighter at the end of September.

Invested in our future capabilities by financing a new $27M maintenance facility at Fort Lauderdale International Airport.

Financial Health and Liquidity:

Closed the quarter with a solid liquidity position, having $17.3M in cash and restricted cash, marking a 46% increase since the end of the previous year.

Financial Outlook:

On the horizon, there are scheduled deliveries for four new aircraft: two A320 passenger planes expected in November and December, and two A321 freighter planes anticipated to arrive in December.

Operational Projections:

The company is on track to achieve over 6,000 block hours of flight in the quarter, indicating robust operational activity.

Performance Guidance and Expectations:

For 2023, the revenue target is set at $150M, which would represent a significant 54% growth over the previous year. Impressively, about 95% of this revenue target, equating to $143M, has already been secured through flown or contracted services.

My Take

The fact that JETMF is expected to take delivery of new aircraft, including two A320 passenger planes and two A321 freighters, is an indication of healthy expansion. This fleet growth allows the company to scale up its operations, meet increasing demand, and potentially enter new markets (keep in mind this is a microcap). This strategic increase in capacity suggests a forward-looking management team that is positioning the company to capitalize on opportunities in both passenger and freight sectors. Also, the significant increase in block hours flown—173% over Q2 2022—is a testament to the operational efficiency and growing demand for JETMF's services. An increase in aircraft utilization by 50% also suggests that the company is effectively optimizing its current assets, which is crucial for profitability in the aviation industry.

Furthermore, the wet lease agreement with TUI, one of Europe's largest leisure carriers, and the substantial increase in government contracts demonstrate their ability to secure profitable and reliable partnerships, which is a key driver for stable revenue streams. Investments in infrastructure, such as the new maintenance facility at Ft. Lauderdale International Airport, illustrate a long-term commitment to operational excellence and capacity building. This will likely enhance the company's ability to maintain its fleet internally, reducing costs and improving turnaround times for aircraft maintenance.

Despite potential challenges in the aviation industry (they aren’t like your commercial airliners), JETMF's ability to consistently record block hours and maintain healthy revenues, coupled with assertive growth initiatives by management, indicates a company on an upward trajectory. With a clear strategy for expansion, a strengthening operational base, and a solid financial position, the business appears well-equipped to continue its growth and potentially become a leading player in its market segment. With no analyst coverage and being an under-the-radar stock, they may have significant untapped potential for investors. As the company continues to deliver strong results, it may eventually attract the attention of analysts and investors, leading to an increase in stock liquidity and potentially a re-rating of the company’s market value. For me personally, I plan to add more to my position in 2024.