Is Palantir's Remarkable Rally at Risk Due to Recent News?

Taking a Look at Palantir Technologies (PLTR), Weekly Activity, & Portfolio Update.

This week, I'm focusing on a stock that's been making waves in the market: Palantir Technologies (PLTR). Recently, there's been considerable buzz around PLTR, especially regarding the potential devaluation of their Army contract renewal. Following widespread coverage in mainstream media and social platforms, PLTR's share price experienced a notable decline, dropping just over 15% in a single week. Despite questions about the company's initial valuation, it seems this news may have been excessively amplified. Let's dive in and explore why this reaction might have been an overreaction.

I do not own shares in Palantir Technologies (PLTR).

A Crossroads of Renewal or Discounted Terms?

2023 has been an excellent year for PLTR, experiencing a remarkable rally, almost tripling in value, driven by investors' enthusiasm for the potential of artificial intelligence solutions. The surge in interest was particularly sparked by the April unveiling of PLTR's new Artificial Intelligence Platform (AIP). Alex Karp, the founder and CEO of PLTR, confidently stated that the company and its software were ideally positioned for this moment in technological evolution. This sentiment was echoed by Wedbush analyst Dan Ives, who likened PLTR to the "Messi of AI," suggesting that the company has established an unparalleled AI stronghold.

However, opinions on PLTR's prospects are not unanimous. Notably, PLTR's stock witnessed a 15% drop (for the week) following remarks by William Blair analyst Louie DiPalma, who maintained his bearish stance on the AI analytics provider. DiPalma's outlook was influenced by uncertainties surrounding a significant contract renewal with the Army. This development, he suggested, could potentially lead to complications and contention.

DiPalma's skepticism partly stems from the possible data ownership conflicts indicated in a U.S. Army presentation at a recent industry event. Without directly naming PLTR, the Army project manager hinted at issues with the current vendor of the Army Data Platform (formerly the Vantage dashboard), a contract held by PLTR since December 2019. The impending end of this contract, worth approximately $458M, raises questions about its renewal terms, with DiPalma predicting a potentially reduced valuation.

Despite this, DiPalma reiterated his view that PLTR's valuation, which was currently at a high multiple of 120 times the estimated 2023 FCF, might align more closely with industry standards, possibly compressing to a mid-30s multiple. This adjustment reflects the broader market metrics for analytics software providers.

The future for the company and its investors is loaded with both opportunity and uncertainty. While the company's valuation is undeniably steep in my opinion, and the potential reduction in revenue from the Army contract is a concern, there are also positive signs. The company recently announced its fourth consecutive quarter of net income profitability under GAAP, a milestone that could pave the way for its inclusion in the S&P 500.

Furthermore, PLTR is successfully diversifying its revenue streams beyond government contracts, which now constitute about just slightly over 50% of its total revenue. The company's government revenue increased by 12% to $308M in the last quarter, while commercial revenue saw just over a 20% hike to $251M. This growth is notably evident in the U.S. commercial sector, which grew by 33% to $116M. Karp highlighted the progress in his latest shareholder letter, attributing it to the demand for the recently launched AIP.

While the U.S. Army contract renewal remains a potential issue, PLTR's strengthening position in the commercial market and its recent profitability streak suggest that concerns regarding this single contract is likely overstated. As the company continues to expand and solidify its commercial foothold, the company's growth trajectory could very well validate its current market valuation.

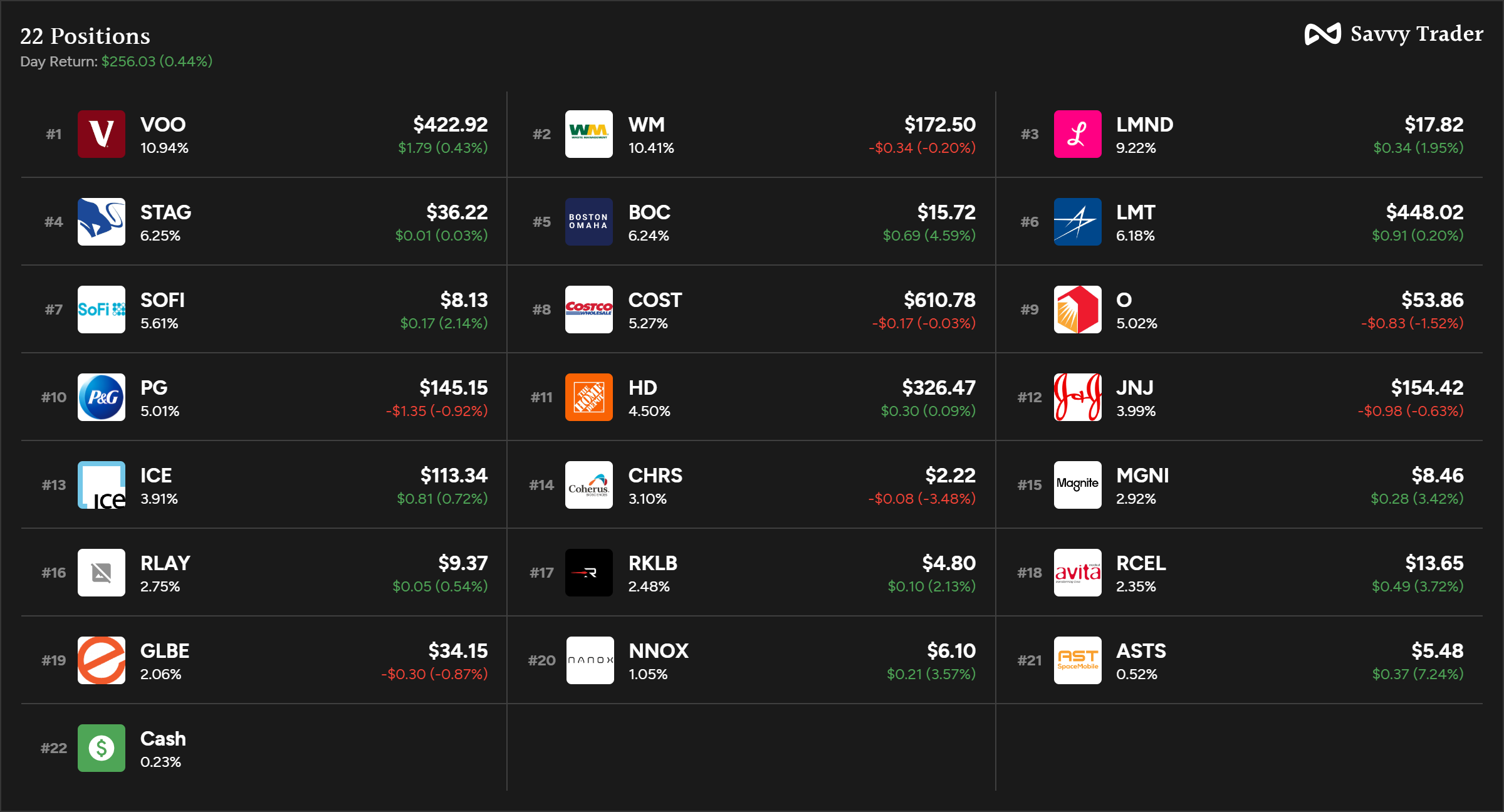

Weekly Activity (December 4th-8th)

1 share of VOO (S&P 500)

5 shares of Realty Income (O)

5 shares of Boston Omaha (BOC

Portfolio Update