My Stance Heading into Coherus BioSciences' Earnings

Taking a Look at Coherus BioSciences (CHRS).

What’s Next for Coherus BioSciences?

Coherus BioSciences (CHRS) has tested my patience for a while now. I initially pegged it as a special situation turnaround, but lately it’s starting to look like a potential turnaround and/or arbitrage opportunity. I want to be absolutely clear: I’ve gone on record multiple times about my stance on CHRS, and I’m not trying to shift the goalposts—I’m just trying to stay reasonable. One thing is for certain, though: assuming Udenyca is divested on paper, CHRS is still undervalued for a commercial-stage biotech. I’ll explain why in a moment.

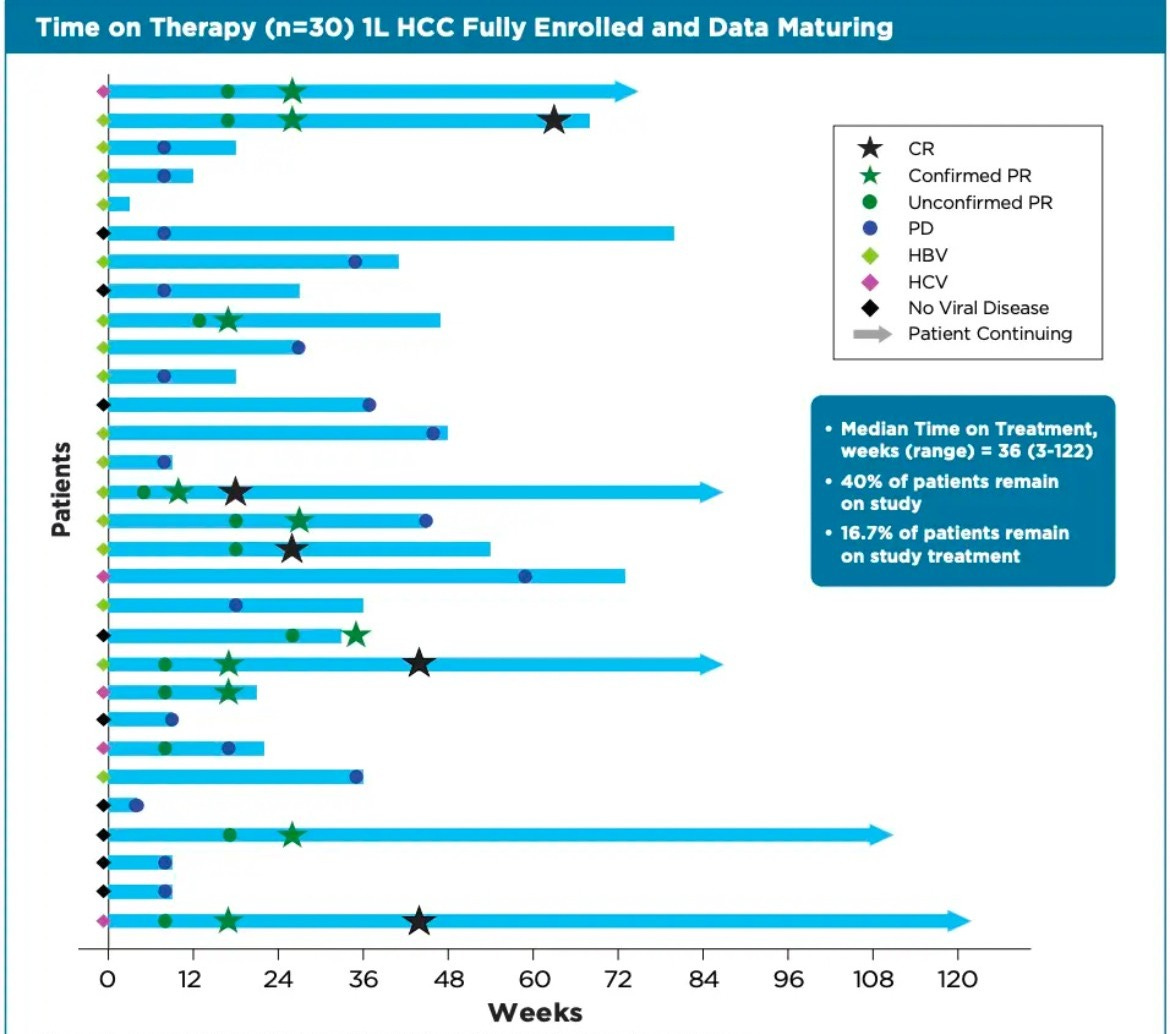

First, let’s talk about the recent Casdozo readout. Contrary to what some might assume, it really wasn’t bad at all. What Casdozo needs most is a larger patient population to see if the efficacy holds steady. Hopefully, we will see this with combination Toripalimab (maybe better overall). Below, I’ll walk through an overview of Casdozo and then compare it side by side with the standard of care (SOC) at the same stage.

Combination Therapy: Casdozokitug (IL-27 antibody) was tested with atezolizumab (PD-L1 inhibitor) and bevacizumab (VEGF inhibitor) in treatment-naïve patients with unresectable or metastatic hepatocellular carcinoma (HCC).

Efficacy Results:

Overall Response Rate (ORR): 38% (higher than the previously reported 27%).

Complete Response (CR): 17.2% (initially reported as 10.3% and 0% at first assessment).

Median Progression-Free Survival (PFS): 8.1 months (per RECIST v1.1).

Disease Control Rate (DCR): 58.6%.

Safety Profile: The treatment was well tolerated, with no new safety concerns beyond the known adverse effects of atezolizumab and bevacizumab.

Significance: The results showed increased depth and durability of responses, supporting further clinical trials. A new Phase 2 trial is now enrolling patients to test casdozokitug in combination with toripalimab (another PD-1 inhibitor) and bevacizumab.

These are good numbers, and it’s actually better than the SOC when it was at this stage, which you’ll see in just a moment. But one thing that should be noted is that there were two PRs that turned to CRs which is great to see. So, two patients when from tumor shrinkage to no tumor detection.

When we look at the SOC side by side with Casdozo during the same period, the numbers are ultimately better.

The most widely accepted first-line SOC for metastatic or unresectable HCC is the combination of atezolizumab (PD-L1 inhibitor) and bevacizumab (VEGF inhibitor) based on the IMbrave150 trial.

IMbrave150 (Atezolizumab + Bevacizumab) Results:

Overall Response Rate (ORR): ~27% (per RECIST v1.1)

Complete Response (CR): ~5.5%

Median Progression-Free Survival (PFS): ~6.8 months

Median Overall Survival (OS): ~19.2 months

Safety Profile: Well tolerated but with a risk of bleeding (due to bevacizumab), hypertension, and immune-related adverse effects

So, Casdozo, in combination with atezolizumab and bevacizumab, actually demonstrated improved efficacy compared to the SOC. The ORR was notably higher at 38%, with a CR rate of 17.2%, compared to the SOC, which showed an ORR of approximately 27% and a CR rate of 5.5%. In terms of tumor control, Casdozo also extended the PFS to 8.1 months, compared to 6.8 months with the current SOC. PFS matters a lot here in oncology trials so this is notable. Importantly, the safety profile remained comparable, with no unexpected safety signals emerging, indicating that the addition of Casdozo did not significantly increase toxicity. Also, DCR looked higher with consistency, which combines Stable Disease (SDs), this is a good sign.

RDCF Valuation

That said, here’s what I really want to dive into in the rest of this article: how CHRS looks from a valuation perspective right now, what might change when Udenyca is effectively taken off the books, the company’s longer-term outlook, and finally, the strategy I’m planning to use as we move forward.

Biotech valuation is often tricky, especially for pre revenue businesses. However, CHRS is indeed a commercial stage biotech company, so unconventionally I’m taking a different valuation approach/perspective by putting them through a Reverse Discounted Cash Flow model since they are generating revenue and have some solid growth projections for the Loqtorzi franchise. After that, I’ll also whip up a quick-and-dirty valuation under a “pre-revenue” assumption—similar to what I’ve done before (no real changes there). This way, we can get a sense of how CHRS stacks up from two different angles.

RDCF model for CHRS evaluates the future FCF assumptions currently priced into the stock at its market capitalization of approximately $130M. As a commercial-stage biotech company, Coherus' value is driven by the expected revenue expansion of the Loqtorzi franchise and the potential contributions from pipeline assets such as Casdozo and CHS-114.

The model assumes a fully diluted share count of 138 million and a net cash position of $200M (conservative), expected to fund operations into the second half of 2026. With no debt, financial risk is reduced. A 15% discount rate (WACC) was applied to future FCF to account for regulatory, commercial, and competitive risks, as well as potential dilution beyond 2026. Larger, diversified biopharma companies typically have a WACC of 8–12%, while smaller commercial-stage biotech firms with growth potential and execution risks tend to fall in the 15–20% range.

The forecast spans 2024 to 2033, capturing Coherus’ transition from negative cash flow to profitability. This will assume they have cash burn of $16–$20M per quarter on R&D and commercialization efforts, leading to negative FCF through 2026. By 2027–2028, break-even FCF is expected as Loqtorzi expands into additional indications, driving revenue growth. Continued FCF acceleration is projected from 2028 onward, supported by Loqtorzi’s market expansion and pipeline contributions. By 2033, projected FCF reaches $240M.

To determine long-term intrinsic value, a terminal value multiple of 10x was applied to 2033’s FCF, resulting in a terminal value of $2.4 billion before discounting. This multiple aligns with industry standards for specialty biopharma firms with sustainable cash flows. Profitable biotech companies typically trade at 8–12x forward FCF, making 10x a reasonable assumption for a company successfully commercializing multiple oncology therapies (they are great on this front).

The RDCF model suggests a fair intrinsic value of approximately $6.48 per share, significantly higher than the stock’s current price range of $1.05–$1.50. At this valuation, the market appears to discount Loqtorzi’s growth potential and the probability of pipeline success.

RDCF models provide insight into what level of future FCF is implied at today’s stock price and are particularly useful for companies in transition, moving from clinical development to commercial profitability. Which I believe is a reasonable model to run, especially from another valuation perspective. Unlike traditional DCF models, which are more commonly applied to large-cap biopharma with stable cash flows, this RDCF model helps assess whether a company’s stock is undervalued given its revenue trajectory, market opportunity, and risk profile.

The most sensitive variables in this valuation are the terminal multiple (8–12x range), discount rate (15%), and the timing of FCF breakeven (this is difficult to pin point). If CHRS successfully expands Loqtorzi’s market share, with more indications, and secures approvals for pipeline candidates, the current share price represents a significant undervaluation relative to its long-term cash flow potential.

Sum-of-the-Parts (SOTP) Valuation

Based on the SOTP model, the total valuation of CHRS is estimated at $630M, significantly higher than its current market capitalization of around $130M. This valuation includes a risk-adjusted pipeline value of approximately $500M, derived from Loqtorzi (NPC and SCLC), Casdozo (HCC and NSCLC), and CHS-114, with adjustments based on the POS at each clinical stage. Additionally, the company’s $200M in cash reserves contributes to the valuation, offset by an estimated $70M cash burn over the next 2ish years (being generous here). Compared to its current market cap, this SOTP valuation suggests an upside potential of approximately 385%, reflecting the significant value of the pipeline and cash on hand relative to its current share price. Again, this assumes Udenyca divested. Roughly, this is another perspective, and I was quite generous with cash burn. I believe it will be consistent above/around $20M and cash reserves are projected to be $250M but I went conservative at $200M.

With the most conservative projections (putting above models aside), we have at least a fair value of around/above $2.00 per share. Either way, CHRS is undervalued and is being neglected.

Udenyca Divestment

I think when this franchise is recorded as closed on paper, we will see the stock price either correct rapidly to a reasonable fair value or gradually make its way there over time. The market is treating CHRS as it’s on the highway to bankruptcy and complete failure which should not be the sentiment right now. This company still has a short interest that is hovering around 30%, which it seems many of these shorts have not covered because they are hedged with corporate bonds which are still outstanding. Once this deal is closed, albeit speculatively, these bonds will be eliminated causing shorts that have been hedged to likely cover their positions. Much of the short campaign is gone, what loomed the company was primarily debt and supply issues with Udenyca. However, this is all irrelevant now with sale being closed. This is something to keep an eye on. The vote looks likely to be a day before their estimated earnings on March 12th (Management hasn’t confirmed this yet**).

Arbitrage Opportunity

I’ve said before that selling off Udenyca never really sat right with me. Given how valuable CHRS’s IPs in pipeline appears to be, there’s a very real possibility the company could be acquired. I won’t pretend to know what sort of price tag that might come with, but it’s definitely worth keeping an eye on.

What started as a straightforward special-situation turnaround has, in my view, morphed into a potential arbitrage opportunity. Others might disagree, but from where I’m standing, CHRS still has enough inherent value to warrant a second (or third) look.

Thesis Has Changed, But Long-Term Value Is Noticeable

The original thesis for this company has changed again. CHRS is transitioning into a full fledge immuno-oncology company, which now seems they are exiting the biosimilar space.

The core thesis now centers on Loqtorzi and the hope of expanding its use beyond just NPC. Currently, it’s the preferred treatment for NPC, and that market is set to grow nicely—especially with a new CMO focused on doubling capacity and Coherus’ strong record of commercial execution. But the real upside with Loqtorzi lies in branching out into more indications.

CHRS has earmarked a sizable TAM for all of its IPs, and a successful push into additional indications for Loqtorzi alone could realistically bring in annual revenues of $300–$500M. Naturally, that’s assuming all necessary approvals come through, but the existing Toripalimab data really boosts the likelihood of success. While exact timelines are still up in the air, it’s reasonable to think we might see these expansions come to fruition in the latter half of the decade.

If everything goes according to plan—and they manage to capture the realistic addressable market—CHRS could feasibly hit a market cap north of $5B. Whether they actually get there is still an open question, but the consistently strong Toripalimab data makes a compelling case for long-term value.

Personal Strategy with Coherus

I’ve said it before and I’ll say it again: this investment has been downright frustrating. Still, I’m sticking to the plan I outlined in previous articles. My goal is to find a good exit point for half of my position, which comes to 10,250 shares. Given my cost basis—initially above $3, but eventually down to $0.98—I’m not in a hurry, and my timing depends on how things shake out. A reasonable exit could be after the Udenyca sale is finalized, but either way, I plan to let go of half my shares at some point. For the other half, I’m hanging on but staying vigilant. If management does anything that derails the Loqtorzi thesis, I’ll be out faster than you can say “sell.”

As for the upcoming earnings call (whenever that gets scheduled), there are a few big things on my watchlist. First, I want to see how Loqtorzi performs in the NPC market. Then, there’s the matter of Udenyca revenues, especially given the recent supply issue—though that may not mean much if they’re truly divesting it. I’m also expecting analysts to dig into the company’s 2025 guidance. We heard a bit about it at the JPM conference, but we need more clarity. And finally, I’m hoping for an update on enrollment for the Casdozo, Toripalimab, and Bevacizumab combo in Phase 2. They’re expanding it to a 72-patient population, which should give us a clearer idea of its potential. Of course, cancer trials can be tricky, so I wouldn’t be surprised if we see delayed enrollment.