Relay Therapeutics Approaching Deep Value Territory

Taking a Look at Relay Therapeutics (RLAY).

I've transitioned to exclusively logging my weekly activity and tracking my portfolio in real-time on Savvy Trader.

For those not yet in the loop, I invite you to join me on this journey. Subscribe using the link below to gain direct insights:

By subscribing, you'll engage directly with me regarding specific companies, access my performance in real-time (with data starting just over a year), and get detailed views of my investments, real-time trading actions, cash positions, and more. This move is driven by my commitment to transparency. I believe that sharing my analytical insights and the reasoning behind my investment choices offers immense value, empowering you with the information you need to make informed decisions.

Eli Lilly Acquires Relay Competitor: What Does This Mean for Relay's Value?

At the beginning of this week, the largest pharmaceutical company in the world, Eli Lilly (LLY), announced a press release that they were going to buy Scorpion Therapeutics for $2.5B. The terms of the agreement is an upfront cash payment of $1B and the up to an additional $1.5B in milestone payments.

So, why does this matter to Relay Therapeutics (RLAY)? As I’ve highlighted in previous updates, Scorpion is a direct competitor to Relay. Both Scorpion and Relay are developing mutant-selective PI3Kα inhibitors—STX-478 and RLY-2608, respectively—targeting cancers with PIK3CA mutations, particularly in hormone receptor-positive (HR+)/HER2-negative breast cancer.

For more details about Relay Therapeutics (RLAY) this program/agent, please refer to articles dedicated to the company in archives.

Historically, PI3K inhibitors have faced skepticism in the oncology community due to their adverse effects, with hyperglycemia being one of the most significant and common issues. Why is this so bad? Well, this can significantly fuel cancer growth, because cancer cells thrive on glucose. These cancer cells have a high demand for glucose due to their reliance on “aerobic glycolysis”, also known as the Warburg effect. This process allows cancer cells to preferentially metabolize glucose into lactate, even in the presence of oxygen, enhancing their rapid growth. Elevated blood glucose levels, as seen in hyperglycemia, provide an abundant supply of this “fuel”, enabling cancer cells to thrive.

In addition to directly fueling tumor growth, hyperglycemia can alter the tumor microenvironment in ways that promote cancer progression. It enhances inflammation and angiogenesis (the formation of new blood vessels), which supply tumors with the nutrients and oxygen needed for further expansion. At the same time, hyperglycemia can impair the immune response, reducing the body’s ability to fight cancer effectively. On top of that, studies have shown that hyperglycemia can decrease the effectiveness of cancer treatments such as chemotherapy, radiation, and targeted therapies, by promoting cellular mechanisms that help cancer cells survive and adapt.

So, all in all, hyperglycemia is NOT good when creating therapies to treat cancer. It is the boogeyman here. Controlling this is crucial when treating cancer patients, especially with traditional PI3K inhibitors, which are notorious for worsening glucose dysregulation. That’s where Scorpion and Relay come in. Both companies are taking a fresh approach with mutant-selective PI3Kα inhibitors like Relay’s RLY-2608 and Scorpion’s STX-478. By adopting this strategy, they can tackle the problem at its root—selectively targeting cancerous cells while sparing healthy ones. *So far*, this approach seems to be working, reducing the risk of hyperglycemia and its harmful effects, and paving the way for safer and more effective cancer treatments.

In the past, many companies have failed to show that the traditional PI3K inhibitor pathway works. Eli Lilly being one of them when they discontinued LOXO-783, but being a massive company like LLY, they had another PI3ka inhibitor agent in their pipeline (Actually, two now if we count Scorpion). The company is now focusing on a next-generation asset, LY4045004, described as a "pan-mutant-selective" inhibitor. Unlike LOXO-783, LY4045004 is not specific to a single PI3Kα mutation but spares the wild-type enzyme, potentially reducing associated toxicities. This molecule originated from Petra Pharma, which Lilly acquired back in May 2020.

Petra Pharma’s story is interesting. It’s not 100% sure that Lilly will/is implementing this approach, but they focused on fasting (like intermittent fasting) along with supplying their agent. The idea was to starve cancer cells through fasting and introduce a PI3K agent. Sounds barbaric, but studies have shown fasting in this context with cancer cells may work. In the fight against cancer, trying anything that could show promise can be looked at as acceptable.

Why STX-478?

Clearly, Eli Lilly has a lot of confidence in the PI3K pathway with the announcement of Scorpion, bolstering their pipeline even more. But why is their eye on the prize of STX-478? Around the same time as Relay presented their Phase 2 results for RLY-2608, Scorpion released interim results on STX-478 for Phase 1 in monotherapy. Meaning this was data presented halfway or more than halfway through phase 1 dosage of just STX-478 and no doublet combination like RLY-2608. Those results weren’t bad for mono, STX-478 showed an Overall Response Rate (ORR) of 21% in all evaluable tumors (n=43) and 23% in HR+/HER2- breast cancer patients (n=22). The Disease Control Rate (DCR) was observed to be 67% overall. In terms of safety and tolerability, STX-478 demonstrated an “ok” level. There was a 10% incidence of Grade 3 ALT/AST elevations at higher doses, indicative of liver toxicity; however, these events were asymptomatic, transient, and apparently reversible after dose interruptions but nonetheless a concerning escalation, even though this is monotherapy, that is a scary statistic moving ahead. Notably, no Grade ≥3 hyperglycemia events were reported. Other common treatment-related adverse events (TRAEs) included fatigue 30% and nausea 20%.

I think Eli Lilly found STX-478 attractive because, even though its monotherapy dose is much lower than RLY-2608—which raises questions about its toxicity profile—it still showed a strong response rate. Lilly probably sees the toxicity as manageable, though I’m skeptical: of course a super-low dose means fewer adverse effects. Still, Lilly might believe they can keep the toxicity under control even if they bump up the dosage. This could end up being a brilliant move for Lilly or it could be a dud—we just don’t have enough data yet. My guess is they wanted to acquire STX-478 before more data comes out, betting on its success down the line.

Some people wonder why Lilly didn’t just go after Relay. Well, there are two main reasons:

Relay would cost a lot more because it’s further along than STX-478 and already showing excellent results heading into pivotal studies. Relay’s data gives it a success probability of 60%.

Who said Relay is even for sale? Companies need to act in the best interest of their shareholders, and Lilly might’ve had to shell out a fortune to convince Relay to sell.

At the end of the day, a lot of this is guesswork, and we just need to stay reasonable about it.

STX-478 vs. RLY-2608

Scorpion Therapeutics - STX-478

Clinical Stage: Phase 1 trial nearing completion. Transitioning from Phase 1 to Phase 2; currently being tested as a monotherapy.

Efficacy:

Overall Response Rate (ORR):

21% in all evaluable tumors (n=43).

23% in HR+/HER2- breast cancer patients (n=22).

Disease Control Rate (DCR): 67% overall.

Safety and Tolerability:

Adverse Effects:

Liver Toxicity: 10% incidence of Grade 3 ALT/AST elevations at higher doses, which were asymptomatic, transient, and reversible after dose interruption.

Hyperglycemia: No Grade ≥3 events.

Other common treatment-related adverse events (TRAEs): Fatigue (30%) and nausea (20%).

No treatment discontinuations due to adverse effects.

Additional Insights:

Monotherapy: STX-478 is being evaluated as a standalone treatment to demonstrate its independent efficacy and safety profile.

Mutant-selective PI3Kα inhibition minimizes wild-type toxicities, such as hyperglycemia, rash, and diarrhea.

Relay Therapeutics - RLY-2608

Trial Name: ReDiscover Trial, focusing on HR+/HER2- metastatic breast cancer and other solid tumors.

Clinical Stage: Completed Phase 1/2 dose-escalation and dose-expansion cohorts. Preparing to initiate a pivotal Phase 2 trial in second-line breast cancer in 2025.

Therapy Type: Doublet therapy, combining RLY-2608 with endocrine therapy, such as fulvestrant or CDK4/6 inhibitors.

Efficacy:

Overall Response Rate (ORR):

39% in the 600 mg BID + fulvestrant group (n=31).

67% ORR in patients with kinase domain mutations (n=15).

Progression-Free Survival (PFS):

9.2 months median PFS for all patients.

11.4 months median PFS for second-line patients.

Safety and Tolerability:

Adverse Effects:

Hyperglycemia: Rare Grade 3 events (2.5% at 600 mg BID).

Other TRAEs:

Fatigue (31% at 600 mg BID, with 9.4% Grade 3).

Diarrhea (35.9%, with 3.1% Grade 3).

Minimal liver-related toxicity reported.

Additional Insights:

Doublet Therapy: RLY-2608 is being tested in combination with other therapies, leveraging its potential to work synergistically and attack multiple pathways in HR+/HER2- metastatic breast cancer.

Designed as an allosteric, pan-mutant PI3Kα inhibitor, RLY-2608 aims to enhance efficacy with good tolerability and minimal wild-type toxicities.

Triplet data should be released sometime soon, but this seems to be a bit anticlimactic listening to management.

A couple of things stand out to me: first, Relay is further along in development, giving them a pretty big head start. Second, when you look at dosage and toxicity, Relay has reported some rare cases of hyperglycemia, plus side effects like diarrhea and fatigue—which aren’t major but still need to be managed (focus should be on hyperglycemia). Despite these issues, Relay has a larger patient population, a higher overall response rate, and it’s using a higher dosage. All of this shows just how far ahead they really are. For STX-478, the maximum tolerated dose was established at 100 mg daily during the Phase 1 trial. Higher doses, such as 160 mg daily, resulted in dose-limiting toxicities (basically trying to find the right dosage without increasing toxicity). In contrast, RLY-2608 is administered at much higher doses, particularly in combination (doublet) therapy. A key dose used in the ReDiscover trial was 600 mg twice daily, equating to 1,200 mg daily—over ten times the daily dose of STX-478. It’s hard to give too much of a criticism here because it is a doublet combo but my point of this is to show you how infant STX-478 is. They still have a lot to prove, and right now Relay isn’t just showing more effectiveness—it’s also much further along, heading into pivotal stages. If Relay succeeds, since probability of success increases at these late stages it’s reasonable to say the chances are higher now, they could be on the verge of commercialization while STX-478 trials are still wrapping up.

Where Does Relay Stand on Value?

If you look back at my earlier posts, you’ll see that Relay’s stock initially popped after releasing their results. Then Scorpion came out with their own data, and soon after, Relay announced a strategic public offering—which drove the stock downward to where it is today. Meanwhile, Eli Lilly has been making headlines in this space with Scorpion, adding even more volatility. Honestly, that’s just the nature of the biotech world right now, especially for pre-revenue companies like Relay.

Let’s talk about how Relay Therapeutics is valued. Since they’re a pre-revenue biotechnology company, the valuation mostly comes down to their pipeline data, the realistic markets those therapies can tap into, and their liquidity (especially regarding cash burn for R&D). Let’s start by looking at the acquisition as a baseline: the deal includes a $1B upfront payment and up to $1.5B in potential milestone payments. Basically, the world’s biggest pharma company is assigning a $1B price tag to STX-478—even though it hasn’t finished Phase 1 yet. Meanwhile, Relay is moving into pivotal stages with their doublet, which appears to be a better agent so far and has a higher probability of success. Given that, it’s fair to value RLY-2608 alone at more than $1B—I’m being conservative by estimating $1.25B.

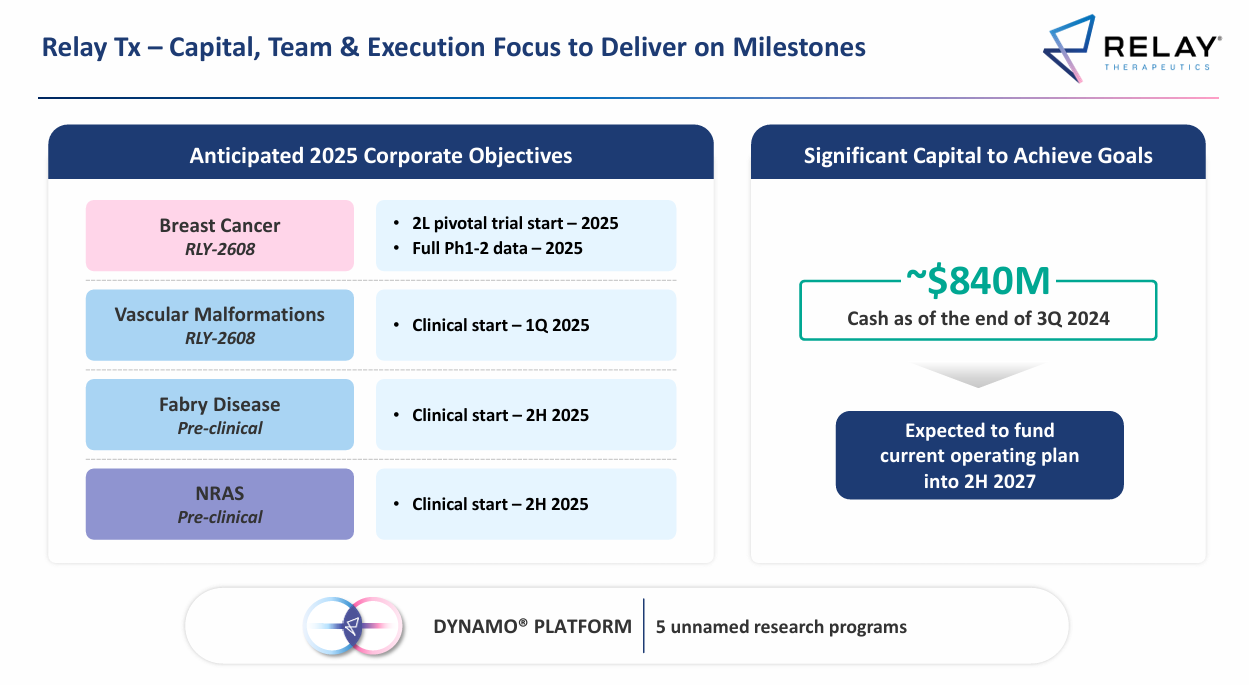

Now, looking at Relay’s cash position, thanks to their recent strategic offering, they’ve strengthened their balance sheet to about $839.6M (roughly $840M if you round it).

Relay expects its current cash to last until the second half of 2027. They’re burning about $75M a quarter on R&D, which is actually down from previous levels because they cut some programs to focus on RLY‑2608. They plan to start clinical trials for their remaining programs in 2025, and their cash projections through 2027 factor in those expenses—though sometimes management can underestimate R&D costs.

By the time their cash starts running low, Relay might already be commercializing RLY‑2608. The realistic timeline for that is end of 2027 or beginning/middle of 2028. They could also form strategic partnerships to help cover commercialization and ramp-up costs. As for market potential, RLY‑2608’s opportunity in breast cancer could be anywhere from $4B-$7B, which some analysts already consider blockbuster territory. It’s not unreasonable to think RLY‑2608 might achieve annual sales of over $1B, especially as a first-of-its-kind treatment for metastatic breast cancer.

The main idea here is to value Relay as it stands right now, not where it might be in the future (that’s a whole different story assuming RLY-2608 is a success). They currently have $840M in cash and a potential market for RLY‑2608 of over $4B. By itself, RLY‑2608 could command a premium valuation of around $1.25B. When you add in their other programs—like Vascular Malformations (which also uses the RLY‑2608 agent), Fabry Disease, and NRAS (not even counting their Dynamo platform)—the company should be worth about $3B in market cap right now. These programs haven’t been touted much by management since their focus is RLY-2608. Below you have the programs and their patient population (US only), you can see Vascular Malformations has the largest market in terms of population.

.

But here’s the catch: despite all that, plus Eli Lilly snapping up STX‑478 for $1B, Relay is trading with a market cap of just $600M–700M. That makes no sense. If a PI3K pathway program that hasn’t even completed Phase 1 can be worth $1B, how is a company with a better therapy heading into pivotal stages worth only $600M—including cash, pipeline data, and conservative market projections?

At the very least, Relay should be trading at $1B now, and that’s still low in my opinion. A $3 B valuation seems more reasonable overall. With 167 million shares outstanding, that translates to roughly $18–21 per share. Personally, I’m going to likely sell my CHRS position (Half) next week upon Casdozokitug data, then put the proceeds into Relay if the valuation sustains (article coming on CHRS before data release next week).