Relay Therapeutics Reports Positive Cancer Results

Taking a Look at Relay Therapeutics (RLAY) Positive Interim Data for RLY-2608.

I've transitioned to exclusively logging my weekly activity and tracking my portfolio in real-time on Savvy Trader.

For those not yet in the loop, I invite you to join me on this journey. Subscribe using the link below to gain direct insights:

By subscribing, you'll engage directly with me regarding specific companies, access my performance in real-time (with data starting under a year), and get detailed views of my investments, real-time trading actions, cash positions, and more. This move is driven by my commitment to transparency. I believe that sharing my analytical insights and the reasoning behind my investment choices offers immense value, empowering you with the information you need to make informed decisions.

Advancing the Fight Against Breast Cancer

Relay Therapeutics’ (RLAY) stock surged nearly 50% after announcing the positive Phase 2 data for its RLY-2608. As I’ve mentioned in previous articles, RLY-2608 is designed to target the PI3K enzyme family, specifically focusing on the PI3Kα subunit, which is encoded by the PIK3CA gene. So, what RLY-2608 does, is it targets patients with PI3Kα-mutated, HR+/HER2- metastatic breast cancer, and the trial's results were great. One of the standout results is a median progression-free survival (PFS) of 9.2 months, which represents the duration during which the condition remained stable and controlled in heavily pre-treated patients. This is a significant outcome that highlights the potential of RLY-2608 in this patient population.

Moreover, RLY-2608 achieved an (ORR) overall response rate of 33%, indicating that a substantial number of patients experienced a significant reduction in tumor size. In my opinion, this demonstrates the drug’s effectiveness, with a durable PFS and a promising ORR. Additionally, 53% of patients with kinase mutations responded to treatment, which suggests RLY-2608 could be viable for this subgroup as well. Importantly, the clinical data also indicates that RLY-2608’s safety profile is comparable, if not better, than that of similar therapies that have already received regulatory approval. Taken together, these results suggest a reasonable pathway to regulatory approval if Phase 3 trials deliver.

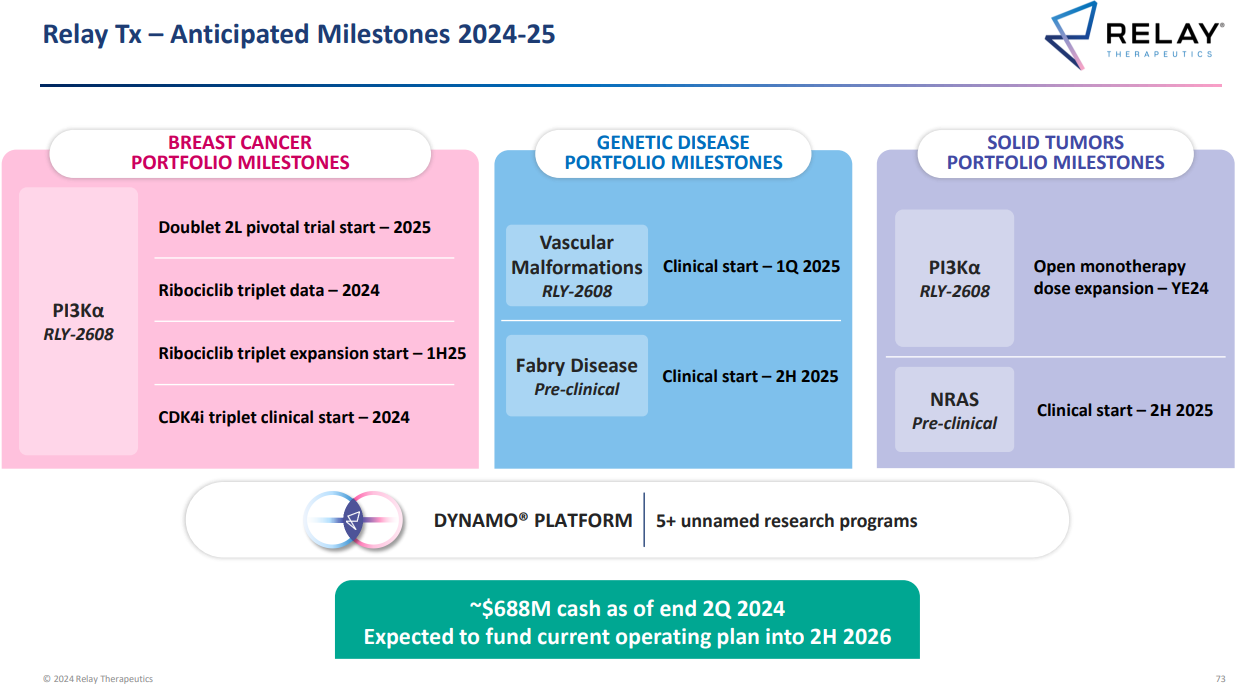

RLAY’s trial data supports the initiation of a pivotal second-line trial in 2025 to evaluate RLY-2608’s efficacy and safety in a larger patient population. Should these results mirror the success of the Phase 2 trial, the drug could potentially secure regulatory approval. Beyond breast cancer though, RLY-2608 is actually set to be tested in various combination therapies and other indications, which could reveal new market opportunities. One of these is a combination of RLY-2608 and fulvestrant, which will be evaluated in breast cancer, with further tests planned in triplet combinations. For instance, in Q4 2024, RLY-2608 will be tested with ribociclib (a CDK4/6 inhibitor) and fulvestrant, with a dose expansion trial expected in the second half of 2025. Another planned triplet combination, to be studied by year-end 2024, includes RLY-2608 with atirmociclib (a CDK4 inhibitor) and fulvestrant. Additionally, by Q1 2025, RLY-2608 will be tested as monotherapy for vascular malformations driven by PI3K pathway mutations, and trials for its use in solid tumors as monotherapy are also expected by the end of 2024.

Naturally, there are risks associated with any investment, and the biggest one here is the potential failure of RLY-2608—a risk that comes with being an investor in biotech. However, as the probability of success (POS) increases, and the odds of failure are indeed decreasing, it’s still important to acknowledge. Another key risk is their liquidity and potential dilution. Currently, RLAY has a solid cash position of $688M, which is expected to grow to nearly $900M following their recent $200M public offering, announced right after their data release.

This brings us to the second risk: further dilution. The $200M offering did cause a recent decline in stock price, but it was a smart move by management. Even though RLAY was fully funded until the 2H of 2026, having additional cash on hand is crucial in biotech, where delays and unexpected challenges often arise, especially for a pre-revenue company. While dilution may create short-term pressure on the stock, it significantly extends RLAY’s cash runway by almost a full year, pushing it to the 2H of 2027. Despite what some say on social platforms, this strengthens the company’s financial position in the long term and should be looked at as a clever move.